Article

How a Mid-Year Business Review Can Impact Year-End

Effective May 21, 2023, P&N has joined EisnerAmper. Read the full announcement here.

Competing needs between current and next-generation leadership create expectation gaps that can be damaging if not properly addressed. Add family business complexities to the mix and the solution becomes even more daunting. In search for a solution, owners can be overwhelmed with countless compensation plans, incentive vehicles, and leadership programs.

How does one find balance? The first step is to have a clear and purposeful strategy that defines the company’s direction and values, and is understood by current and future stakeholders. A clear strategy is critical to successfully navigating employee retention options, particularly long-term incentives

In a world of rapid change, instant gratification, and talent wars, contractors are challenged to maintain profits and retain key employees while incentivizing behaviors for long-term success. This becomes increasingly complex during uncertain economic conditions and is accelerated by a growing number of Millennials poised to enter upper management positions following the wave of Baby Boomer retirements.

Once a strategy is defined and clearly communicated, the next step is to align the overall compensation and incentive menu with the company’s strategy.

Although the focus of this article is on long-term incentives, base compensation and short-term incentives must first be considered. After all, if either base compensation or short-term incentives are not effectively designed, then any attempt to structure effective long-term incentive plans will be futile.

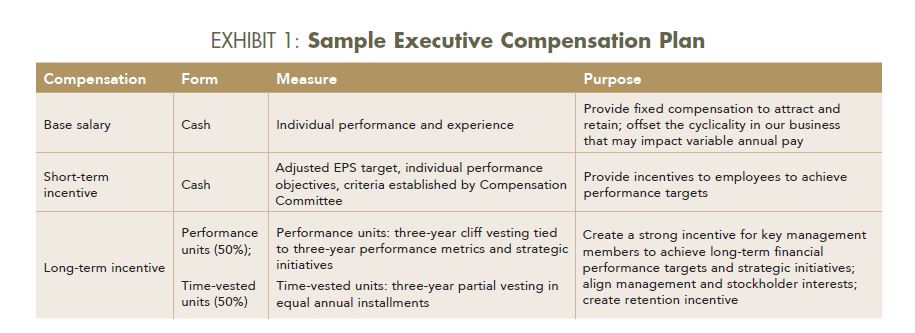

To better understand how a company’s total compensation package can be aligned with strategy, take a look at an excerpt of a public company’s most recent Form 10-K filing: “Our ability to deploy services to customers throughout the U.S., Canada, and Australia as a result of our broad geographic presence and significant scope and scale of services is particularly important to our customers.”

While this excerpt does not depict an entire strategy, one can gather that growth in specialty areas covering expansive geographic markets is critical. Exhibit 1 (below) illustrates how compensation and incentives are aligned with strategy for this same company’s executive compensation plan (Schedule 14A).

Alignment between strategy and plan design is evident in numerous ways:

While this plan applies to named executive officers of public companies, private companies can also use the organization of plan components as a tool to guide decisions on long-term incentive plans for key employees.

Even with a clear strategy, navigating the menu of incentive options can be intimidating. Who should be eligible? How much should be awarded? What are the right performance metrics? Since companies and their strategies are unique, so too are the answers to these questions.

Let’s review common plan aspects and illustrate how to align them with your company’s strategy:

The menu of options can become complicated as each layer is applied, further challenging companies to maintain strategic alignment. Unlike executive compensation plans of public companies, private companies lack accessibility of daily published stock prices to bundle into incentives for equity-based plans. As a result, private company incentive plans may need to include more creative plan designs; however, plan designs should be simple enough for key employees to recognize potential earnings power.

Let’s examine a case study that depicts how strategy can be aligned to the application of long-term incentive plan options for two companies in the same industry with different strategies. Keep in mind that the following is for illustrative purposes only, and actual plan decisions may vary. Additionally, while beyond the scope of this article, decisions on plan options should consider tax consequences for both the employee and employer.

Company A (“Family Company”) is a third-generation family-owned specialty trade contractor in a rural area. Growth is low, but revenues are stable and profit margins are high. Current upper management is composed of only family; next-generation upper management is expected to be a mix of family and non-family. Family Company’s founders and owners are self-educated, and the company has a long-standing passion for providing vocational training in underserved communities.

Currently, Family Company’s incentive program includes subjective annual cash bonuses. Ownership wants to structure an incentive plan that will increase employee loyalty and enable the company to attract external talent if needed.

Family Company’s primary strategic initiatives are:

Company B (“Growth Company”) is a GC that was founded 15 years ago by three non-family partners who ventured on their own. Over the past decade, the company has experienced rapid growth and operates in multiple geographic areas.

Margins are low but stable, and expansion plans include adding key personnel in new markets.

Currently, Growth Company’s incentive program includes annual project bonuses and distributions to owners. Ownership wants to attract and retain new talent, but does not want to provide equity as an incentive. Ownership’s exit plan is to sell to in 7-10 years, and giving up equity can diminish upside earnings potential and create conflicts of interest amongst decision-makers. Ownership, however, realizes that future value will be enhanced by developing management depth.

Growth Company’s primary strategic initiatives are:

Family Company will place select family members into leadership positions early and allow them to grow into the role. Additionally, family members who are not in leadership positions may be nominated into a long-term incentive plan as an alternative to stock ownership. This nomination option minimizes perceived inequities in family salaries and ties compensation to performance.

To further minimize bias, Family Company will establish a Nominating Committee composed of current and prior ownership, trusted advisors, and a representative from its philanthropic organization.

Growth Company is expanding by acquiring talent in new markets. Classification eligibility allows ownership to include each newly hired leader to participate in the long-term incentive plan based on his or her job title (e.g., superintendent, market vice president, etc.).

Partial vesting provides a simple way for Family Company to allow eligible employees to become vested over a defined period of time. Facing increased competition for talent, Family Company elected a shorter vesting period of three years, with 50% vesting in year one and 25% in each of years two and three.

Growth Company is rapidly adding people in new markets, and while ownership is cautious in providing payouts without proven performance, the company needs to attract talent. Growth Company elected a cliff vesting option in which employees are 0% eligible for the first two years and 100% eligible in year three.

Family Company’s operations are relatively stable and profits are predictable. Because certain family employees have higher than average salaries, a percentage of base salary award may not be an equitable method for determining awards. Consequently, Family Company implemented an award opportunity equal to 20% of three-year average annual profits, and the available incentive pool will be allocated evenly among eligible employees (subject to achievement of performance metrics).

Growth Company is rapidly expanding, and annual profits can be unpredictable. Additionally, with an increasing number of eligible participants entering the plan, an incentive pool method may be diluted or difficult to provide consistent award

opportunities. Consequently, Growth Company elected to provide annual award opportunities equal to 20% of eligible employee’s base salary.

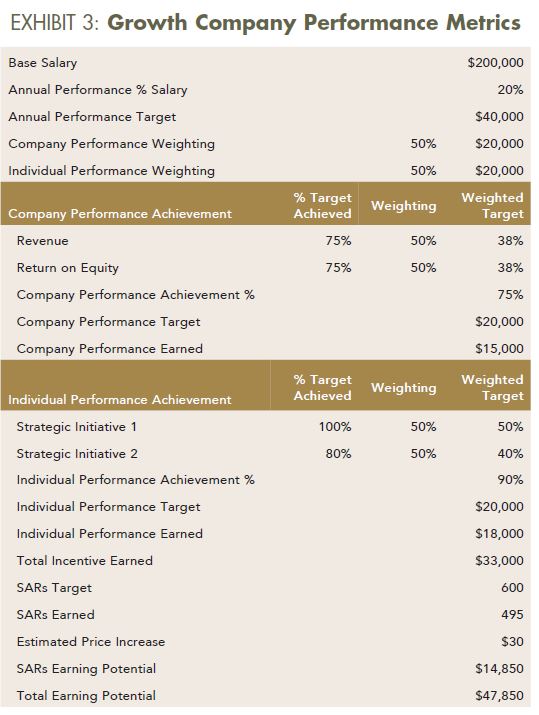

In addition to base salary, Growth Company provided eligible employees with stock appreciation rights (SARs) to incentivize growth in equity value. SARs will be determined in units based on 1.5% of the base salary award opportunity (e.g., base salary = $200,000 x 20% = $40,000 x 1.5% = 600 SAR units). The combination of base salary and SARs is designed to provide higher earnings upside, offset longer-term cliff vesting, and align with the owners’ exit strategy.

Family Company chose to offer cash awards because stock ownership is complicated among family and non-family members. Moreover, given the stability of earnings and limited growth, there is little room for stock appreciation; therefore, cash is considered the primary incentive vehicle. Cash is also considered more attractive to employees than what larger competitors may offer in the form of equity-based awards (stock options, restricted stock, etc.).

Growth Company understands cash is preferred by employees, but it also wants to strongly encourage retention due to high competition for labor. As a result, Growth Company issued a cash award, but a portion of the award will be earned through SARs to provide a retention vehicle.

The value of SARs will be determined based on a three-year measurement period and paid in cash when earned.

Family Company has limited growth opportunities; therefore, owners selected quantitative financial metrics that focus mostly on maintaining stable revenues and profits (three-year average revenues and return on assets). Additionally, as philanthropy is important, Family Company set volunteer hours as its third quantitative performance metric.

As a specialty trade contractor in a rural area, quality of work and customer retention are important to Family Company. Therefore, qualitative metrics are set around customer relationships and employee training and development initiatives. The company elected to give quantitative and qualitative metrics equal weighting in determining incentive achievement, as shown in Exhibit 2 a few pages back.

Expansion and stock appreciation are important to Growth Company; therefore, ownership selected three-year compound annual growth rate and return on equity quantitative performance metrics.

To incentivize growth in new markets, Growth Company elected to include the following qualitative metrics aligned with individual and company strategic initiatives: acquisition diligence, training and development, systems implementation, and facilities management. Growth Company elected to give quantitative and qualitative metrics equal weighting in determining incentive achievement. Additionally, SARs awards will be determined on the same weighting scale. (See Exhibit 3.)

Family Company elected to spread earned cash awards over a three-year period with 50% payout in the first period and 25% in the following periods (similar to vesting). This front-loaded payout is designed to not only be attractive, but also encourage retention by requiring continued employment to receive future payouts.

Offsetting its cliff vesting option, Growth Company elected to payout as soon as fully vested.

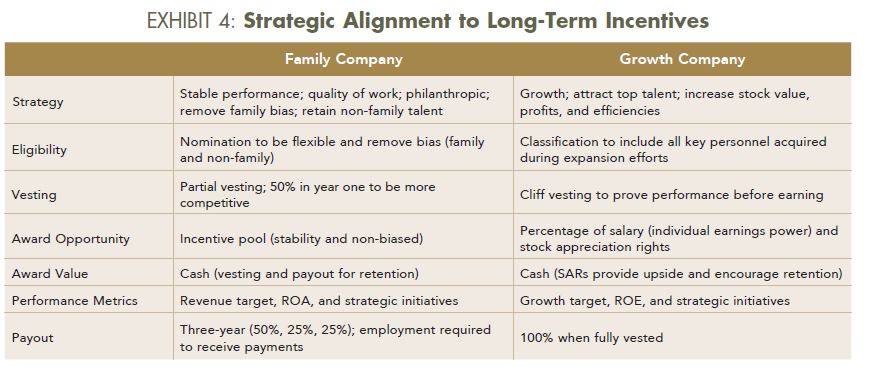

Exhibit 4 summarizes strategic alignment to long-term incentive plans options discussed throughout these examples.

The idea of aligning company strategy with long-term incentive plans is a somewhat simple concept; however, it is often difficult to effectively implement due to the imbalance between long-term strategy, instant gratification, and corporate demands to “meet the numbers.” Company financial officers and decision-makers are nonetheless tasked with finding this elusive balance.

Implementing tactics without a strategy is costly and ineffective, and company leaders should start with a winning strategy.

Compensation and incentive plans can be structured to measure the right targets, encourage the right behaviors, and achieve the desired results. Anything short of that is a gamble, and you are not in control of the odds.

Source: CFMA Building Profits March/April 2017

.jpg)