Article

Form 1099-K Reporting Changes & How to Prepare

Effective May 21, 2023, P&N has joined EisnerAmper. Read the full announcement here.

.jpg)

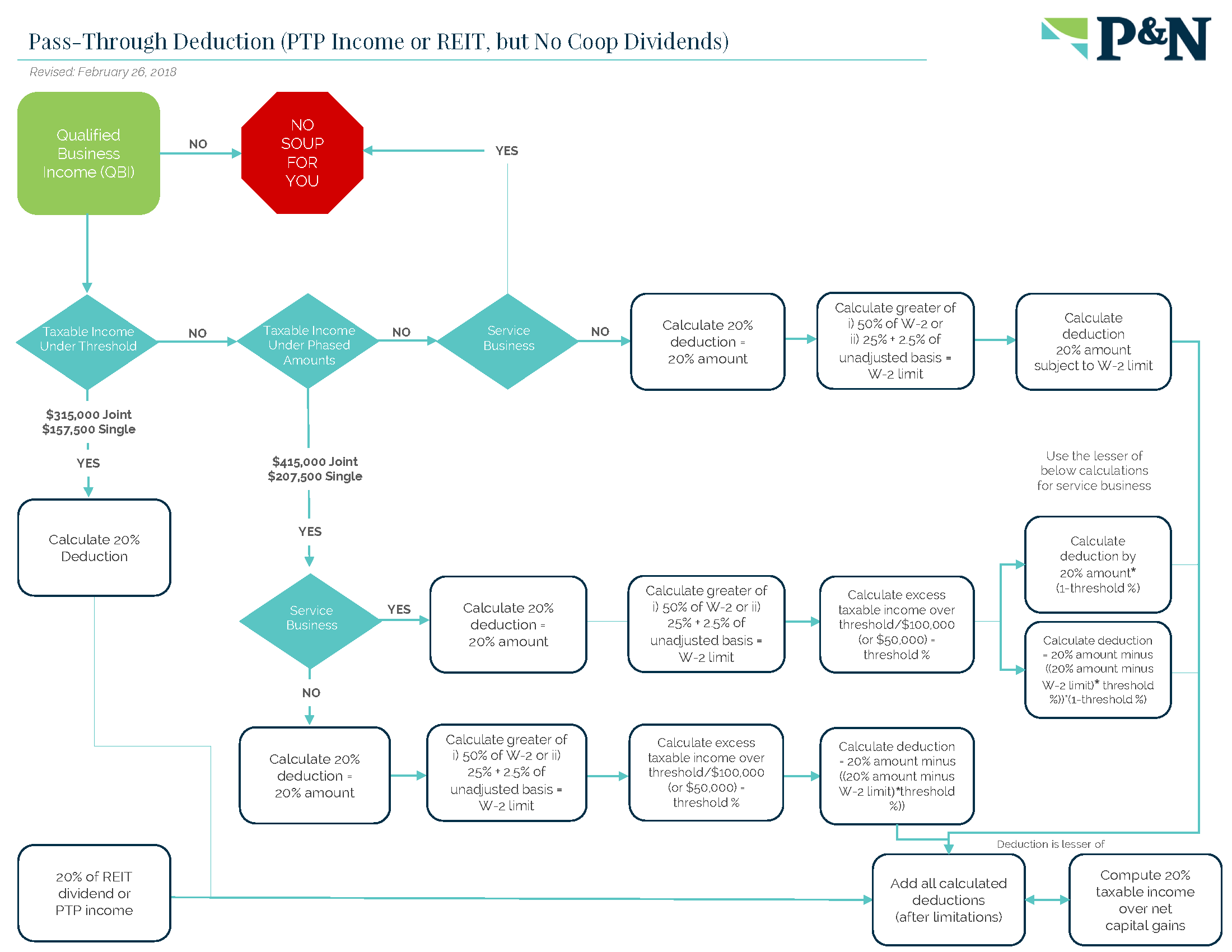

In December of 2017, Congress passed, and President Trump signed, the Tax Cut and Jobs Act which made sweeping changes to the U.S. tax code. One of the more revolutionary changes was the creation of a deduction for owners of pass-through entities. This deduction is equal to 20% of the qualified business income passed through to each partner/member of a pass-through entity. Below, a flow-chart outlines the application of the deduction. However, there are a few key points to remember about the deduction.

The above chart and explanation outlines the general application of this deduction. More guidance is expected to be issued about the I.R.S.’s exact interpretation of the deduction and its application in special situations. As you review this new change to determine its application to your business, please contact your P&N professional for any questions about the how deduction applies to your situation.

If you want to learn more about tax reform or have questions, please visit our tax reform page or contact us.