Article

Closeout of Grant Programs: Best Practices for Timely and Efficient Closeout

Effective May 21, 2023, P&N has joined EisnerAmper. Read the full announcement here.

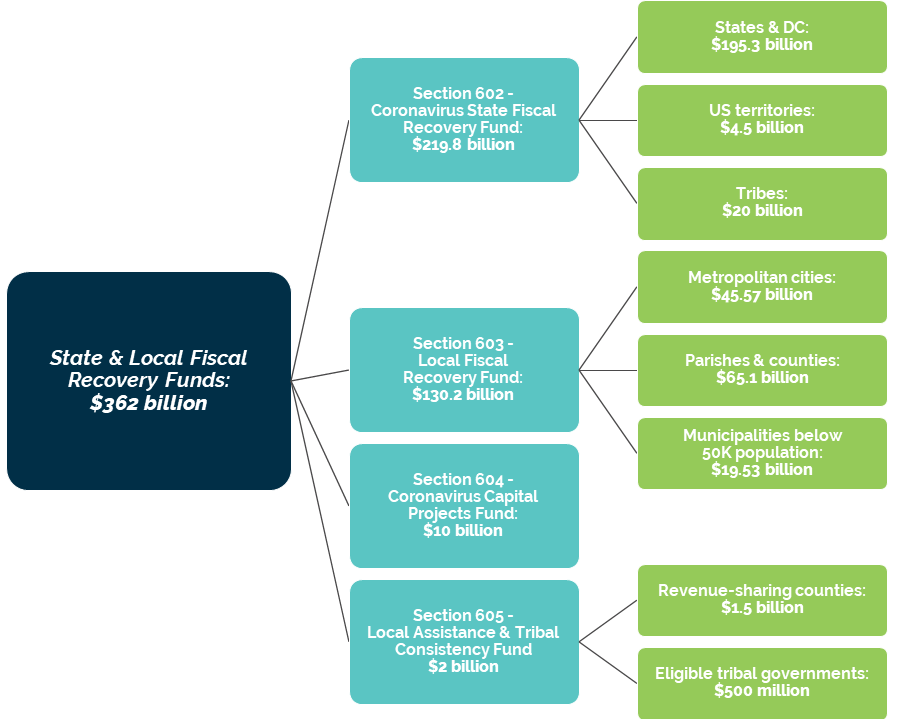

The American Rescue Plan Act of 2021 (ARPA) was signed into law on March 11, 2021. The $1.9 trillion act includes a $362 billion appropriation for the Coronavirus State and Local Fiscal Recovery Funds. These Recovery Funds provide additional resources to help governments recover from the public health and economic crisis resulting from the coronavirus pandemic.

Recovery Funds may be used to cover costs incurred through December 31, 2024 for the following purposes:

As with the Coronavirus Relief Fund established under the CARES Act, its anticipated that the U.S. Department of the Treasury will be releasing further guidance on use of funds.

The ARPA specifically prohibits these funds to be used to make any deposits into a pension fund. In addition, Recovery Funds cannot be used to offset directly or indirectly a reduction in tax due to a change in law, regulation or administrative interpretation, a reduction in tax rate, a rebate, or delays in tax increases.

The following diagram shows the allocation of the Recovery Funds based on state and local assistance and the further allocation by type of government:

The Act specifies how the U.S. Department of the Treasury will allocate the appropriation for each section and when payments are required to be distributed. The following table summarizes the allocation and distribution method for each:

|

States & |

Local Governments: $130.2 Billion |

||

|

$195.3 billion |

$65.1 billion - |

$45.1 billion - |

$19.53 billion - |

|

$25.50 billion, equally divided |

Based on parish/county share of U.S. population in the latest census |

Based on population using the modified CDBG formula |

Based on the proportion of population compared to the total population of all non-metropolitan cities in the state |

|

$168.55 billion allocated based on the proportion of each state's average share of unemployed individuals for the last quarter of 2020 |

Parishes/counties that are recipients of the Community Development Block Grant (CDBG) receive an allocation based on the larger of the share of the U.S. population based on the latest census or the modified CDBG formula |

A “metropolitan city” is defined as a city with a population greater than 50,000 per 42 USC 5302 |

Allocation amount cannot exceed 75% of the most recent budget as of January 27, 2020 |

|

U.S. Treasurer to distribute to each state within 60 days of receiving certification from state |

U.S. Treasurer to distribute a First Tranche (approximately 50%) directly to counties and parishes within 60 days of enactment with the Second Tranche paid one year later |

U.S. Treasurer to distribute a First Tranche (approximately 50%) directly to metropolitan cities within 60 days of enactment with the Second Tranche paid one year later |

U.S. Treasurer to distribute to state |

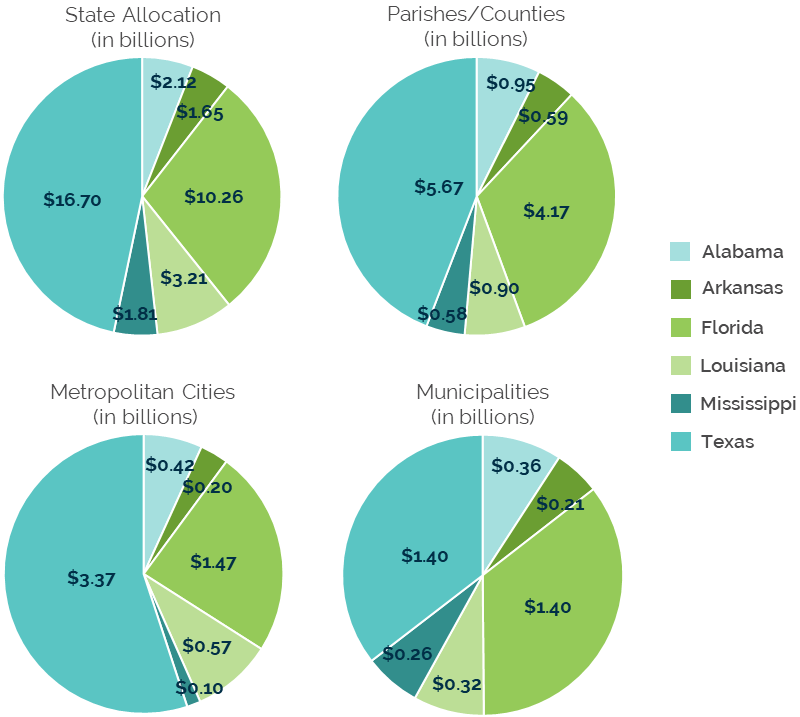

Specific guidance is still pending from the U.S. Department of the Treasury, including details regarding final allocations and when will the funds be distributed. However, the Government Finance Officers Association (GFOA) recently prepared an estimate of the above allocation to states, counties/parishes, metropolitan cities, and municipalities.

The graphs below summarize the GFOA estimates for states in the southern gulf region:

The detailed GFOA estimate can be downloaded here (.XLSX file).

Grants administration – Grants administration and disaster recovery can be a challenging and complex process. Numerous laws and regulations govern the use of program funds, and compliance is paramount for your organization.

Evaluation and planning – Examine existing needs and lay out a strategy for how these funds will be used. Next, develop plans, policies, and procedures based upon this information.

Accounting systems and internal controls – Determine if appropriate resources (personnel and systems) are available to administer and manage the funds. Ask the following questions: Does adequate staffing exist? Can our accounting system appropriately track and report costs? Do our internal controls need to change as a result of this additional funding?

Assistance may be needed – Evaluate whether professional services, such as accounting or legal assistance, will be necessary to help guide you through the above considerations.

P&N has extensive experience in governmental accounting, auditing, and grants administration services and we are ready and available to assist you. Contact us to start a conversation about Recovery Funds available to your organization and the unique challenges that administering these funds may pose.

|

|

|

|